The Impact of Rising Interest Rates

As we settle into the fourth quarter, it makes sense that rising interest rates are the most important topic in real estate. When looking at the average 30-year fixed rate increase in the last ten months, it would be difficult for it not to be the topic of conversation. In mid-January, the average interest rate was 3.45%. Currently, the average rate of a 30-year fixed-rate mortgage is 6.92%. How do rising interest rates impact buyers and the real estate market?

How Interest Rates Impact a Buyer

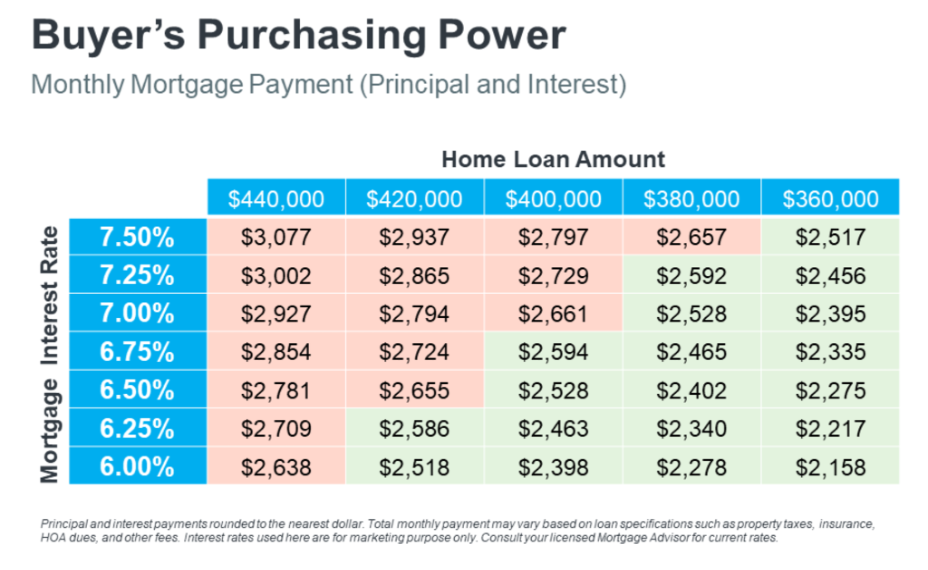

With the ease of online real estate shopping, it is not uncommon for curious buyers to spend their time virtually looking at homes in a dedicated price range they believe they can afford. The price range is a factor in the home-buying process, but the most critical aspect is determining the monthly cost to own a home; this includes mortgage payment, taxes, and homeowners insurance. A lender must establish an approved monthly budget– this monthly budget determines what a buyer is allowed to borrow.

How does the mortgage interest rate impact your monthly budget? In a fixed-rate loan, the interest rate remains unchanged during the loan term and is the percentage of the total loan amount you will have to pay. The loan is amortized over the life of the loan (most commonly 15-year or 30-year), thus establishing a fixed monthly mortgage payment.

Your monthly payment is your purchasing power, your dedicated price range. The higher the interest rate on the mortgage loan, the higher the monthly payment. The lower the monthly payment, the greater purchasing power.

Small increases matter. For each 1% increase in interest rates, the total amount a buyer can borrow declines by approximately 10%.

In addition to the interest rate, other factors can limit what you can borrow— credit history, down payment contribution, and debt-to-income ratio are calculated in determining the monthly payment budget.

Interest Rates, Then & Now

While the current interest rates seem less than ideal, it would be negligent not to provide a brief history of interest rates and how the historically low-interest rates of 2020 impacted Idaho.

A Brief History

By the end of the 70s, mortgage rates rose to double digits at 12.90%. Inflation began to increase quickly in the 80s, and the Federal Reserve forced interest rates to a record high of 18.45%— they remained in the double digits for a decade. By the 90s, interest rates crawled back down to the single digits, sparking a surge in refinancing. Just before the transitional year of 2000, rates fell below 7%. From 2000-2010, rates fluctuated between 5% and 6%, hitting a low of just under 5%. Rates hit a new record low of 3.35% during 2010-2020.

The Impact on the Idaho Real Estate Market

It can be argued that 2020 was the year that set the stage for a significant shift in our country and, more specifically, the real estate market in Idaho. Due to Covid-19, businesses were forced to shut their doors, and remote employment became the new normal. The desire to relocate surged and Idaho landed at the top of the list as one of the most desirable places to live; three of Boise’s suburbs (Meridian, Caldwell, and Nampa) ranked in the top 15 of the fastest-growing cities in the country.

Towards the end of 2020, interest rates hit a historic low of 2.68% for a 30-year fixed mortgage. Record low interest rates, lack of inventory, and the high relocation demand culminated in frenzy buyer conditions. Existing homes were selling at a record pace, resulting in unfavorable buyer terms and over-asking negotiations. In 2020, over 50% of homes sold were over asking, peaking at around 70% in 2021.

Albeit the rising interest rates directly impact purchasing power– the flipside is a market correction, pivoting in favor of the buyer that was sidelined during the highly competitive market just one year ago. Even though anxious buyers welcomed the lower interest rates in 2020-2021, the real estate market in Idaho evolved into a highly competitive seller’s market, and loan approval did not always result in securing a home.

The Market Now

With the current interest rates, you are likely questioning how there could be a benefit or opportunity to purchase a home in today’s market.

Buyer-Friendly Conditions

During the competitive buying frenzy of 2020-2021, in an effort to increase the chances of an offer getting accepted, buyers were often forced to waive all contingencies. Forgoing an inspection and waiving the appraisal was not uncommon. This strategy was typically successful in getting under contract; still, it put the buyer at risk for purchasing a home with possible unknown structural or mechanical issues and/or overpaying for a house that did not appraise for the negotiated contract price.

However, these crucial buyer-protecting contingencies have re-surfaced, shifting the market back to more buyer-friendly conditions.

Cooling Home Prices

Lower interest rates resulted in too many buyers competing in an already historically low inventory of homes. Increased interest rates reduce the number of qualified buyers, which inevitably applies downward pressure on home prices.

In September, in Ada county, on average, buyers paid less than asking through a lower accepted offer, price reductions, or seller concessions.

More Inventory

While “Days on Market” has increased significantly, additional listings are coming onto the market daily. Longer Days on Market, and more inventory mean more time and more choices for qualified homebuyers!

-

2,420 available listings in Ada County, an increase of 93.8%.

-

Average 38 Days on Market in Ada County, an increase of 100%

Lending Option to Reduce Your Interest Rate

Todd Shreeve

Direct: (208) 570-3040

Fax: (208) 995-2139

Address: 2965 E Tarpon Drive, Suite 190 Meridian, ID 83642

2-1 Buydown

A 2-1 buydown program is a financing program designed to reduce your interest rates for the first two years of a mortgage. This program will buydown your interest rate by 2% the first year and 1% the second year.

Although the borrower has a reduced interest rate for the first two years, the interest rate returns to the original interest rate at the third year of the mortgage term.

How Does the Buydown Work?

The builder or seller will fund a temporary buydown in the purchase agreement, negotiated through an experienced real estate agent. This buydown may be in the form of mortgage points or a lump sum deposited in an escrow account with the lender and used to subsidize the borrower’s reduced monthly payments.

A 2-1 buydown is a temporary solution to lower your monthly payment for the first two years— you will want to work with a lender to determine if this specific buydown option is optimal for you.

The Silver Lining

Rising interest rates have impacted buyers as well as sellers, but there is a silver lining. Cooling home prices, strategic mortgage financing, and the return of buyer-friendly conditions are good indicators that homeownership is still attainable.

At the Mike Brown Group, our agents understand that your needs and circumstances are unique to you. We know that it’s imperative that we stay attuned to the shifting market. When the time is right for you, we will be here to help you take advantage of the home-buying opportunities that are hiding in the shadow of rising interest rates.