Many small business owners struggle to pay their taxes each year. That’s why most tax accountants do their best to reduce taxes for their clients. In other words, they find every allowance in the tax code to reduce the income on a business owners’ tax returns. Some even work to show a loss for tax purposes vs profitable income.

Reducing taxable income for a business owner sounds like the work of a fabulous accountant, but sometimes that tactic backfires…especially when the business owner wants to buy a home in the next couple of years.

As a small business owner, you might wonder how your tax filings impact your ability to buy a house. Well, wonder no more!

This article discusses the relationship between taxes and home buying AND we’ll give you tips to share with your tax professional to improve your chances of success when applying for a mortgage.

Quick caveat: we are not tax or financial advisors and this article does not provide tax or financial advisory services. However, we have walked every step of the way with many, many small business owners as they purchase a home and we’ll share what we’ve learned from those experiences with you.

Extra Hoops for the Self Employed

You own your own business. Congratulations! You fuel the American economy. That means you’re living the American dream, right?

As a reward, you’ll have tougher requirements when applying for a mortgage.

We believe small business owners are the most industrious and resilient people around. Lenders, however, see you as a higher risk than those who are employed by others.

Your employees provide a W2 to prove their income in order to qualify for a loan. You? You may need ALL of the following documentation:

- W2s (if you’re an S-corp and pay yourself via payroll),

- bank statements,

- 1040s,

- proof of your estimated tax payments (if any),

- business tax filings,

- business profit & loss statements,

- and your business balance sheet.

But before we hop into some of those bureaucratic hoops created for small business owners, let’s make sure lenders consider you self employed.

Self Employed Defined for Taxes

Fannie Mae and Freddie Mac, our favorite villains in The Big Short, govern lending requirements for most conventional loans. As a result, lenders generally use the Fannie Mae/Freddie Mac guidelines when issuing mortgage loans.

So, when do Fannie Mae and Freddie Mac consider you “self employed?” In other words, when do lenders require you to jump through special hoops before approving your mortgage loan?

Here’s an excerpt from the Fannie Mae selling guide.

“DU will consider the borrower self-employed if the ownership share is 25% or more, or if the ownership share is not completed but the business owner/self-employed indicator is checked.”

? Tip 1: Check the Right Box

That means item one on your tax tip list is to make sure you’re checking the right box. If you’re a co-owner, and you own less than 25% of the business, speak to your tax advisor. Let them know you’re planning to buy a house within the next couple of years. And make sure you have the right business owner information on your tax returns.

The Taxman Cometh, so Make Sure You’ve Filed

For most small business owners (SBOs), the tax filing process is about as appealing as a root canal. But whether you like it or not, filing timely tax documents has a huge impact when it comes to buying a house.

? Tip 2: Get Taxes Current & Pay Penalties

We always suggest using a tax professional to file your taxes as a business owner. But if you haven’t used a professional in the past, and you can’t find your previous tax returns, the IRS provides previous return information online. You can access the IRS online tax portal here.

The IRS online tax portal will show filings, payments, and any recorded overdue amounts. While we’re positive the IRS keeps good records, we encourage business owners to keep their own documentation for at least 7 years. Therefore0, if you notice errors in the IRS online system, you can request a correction with supporting documentation.

On-time filings and payments provide your lender with further proof of your ability to pay your home loan.

So, if you have any outstanding tax filings, payments, or penalties, take care of them pronto.

Small Business Owners’ Ability to Repay

Lenders closely review your personal and business financials to determine your ability to repay a loan. Let’s talk about the different documents you’ll provide based on different financial scenarios.

What Do Lenders Look For in Business Owner Tax Returns?

Lenders follow a decision tree of what documentation they’ll need as outlined by the Fannie Mae and Freddie Mac guidelines.

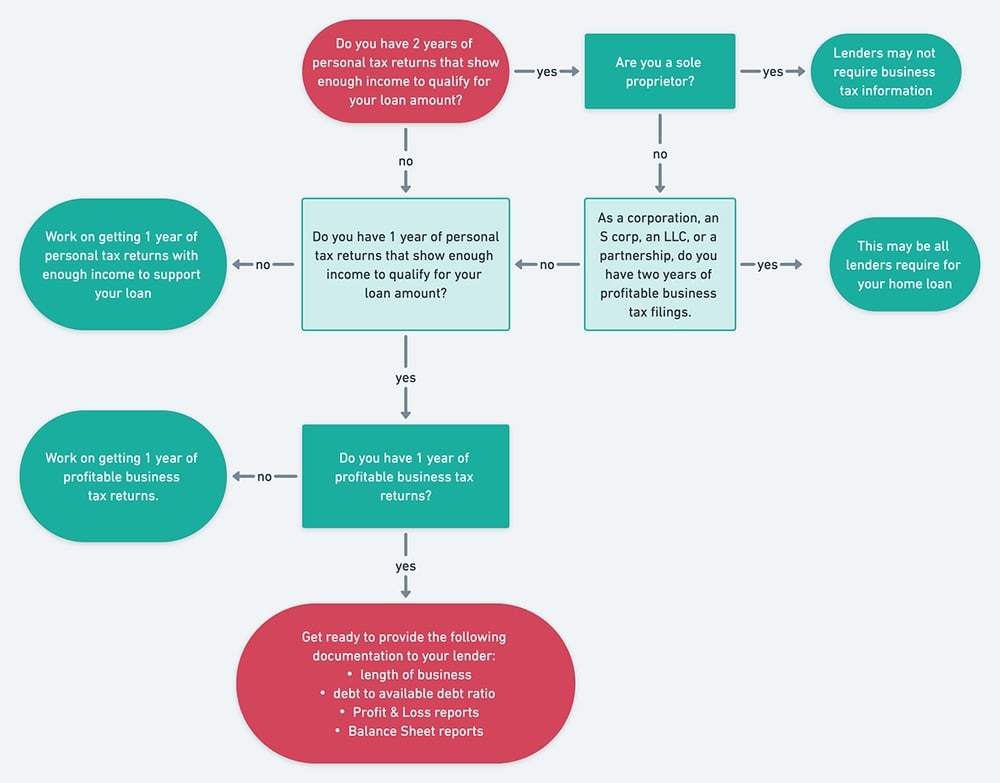

? Tip 3: Get 2 Good Years of Personal Tax Returns Under Your Belt.

Decision 1.a.: Do you have two years of personal tax returns that show enough personal income to qualify for the loan you seek? If the answer is yes, that may be all the information you need. Proceed to decision 1.b.

Decision 1.b.: Are you a sole proprietorship?

If the answers to 1.a. and 1.b. are yes, then you may not need to provide a lender with any business related tax or financial documents.

Decision 1.c.: Not a sole proprietor? You’ll need two years of business tax filings. That means, if you are a corporation, an S corp, an LLC, or a partnership, you’ll need to provide your lender with two years of profitable business tax filings.

? Tip 4: Make Sure you Have 2 Previous Years of Profitable Business Tax Filings.

Which leads us to Decision 2.a.: Does the revenue reported on your two years of personal tax returns support the loan amount you seek? If yes, proceed to Decision 2.b.: Did you report a profit on your two previous years of business tax returns?

Obviously your best scenario includes getting 2 previous years of good reported personal income and 2 years of profitable business income filed. However, if you don’t have 2 years of good business and personal tax filings, don’t give up.

One Good Year of Reportable Income

Maybe you had one bad year of business or personal income. Almost every business owner knows what it’s like to make personal sacrifices to keep the business going.

Or maybe you’ve been using the strategy of taking a business loss on your taxes, so you’ll have less taxable income. Whatever the reason, many business owners struggle to show two consecutive years of healthy personal or business income.

But don’t lose hope. If you need to make a home purchase without waiting another year, you still may qualify for a loan. You’ll just have to find the right lender and provide more documentation that proves you have the ability to repay.

Longevity Equals Stability

This is where business longevity can play in your favor. Most lenders will work with business owners who have kept a business up and running for over 5 years. If you’ve owned your own business for more than 5 years, one good year of reportable business and personal income may save the day.

? Tip 5: Get out of Debt

Even with over 5 years in business, you’ll have to provide more documentation to qualify for a loan. And with only one good year of favorable tax returns on your side, lenders will scrutinize your levels of cash and debt.

To get the best possible interest rates, you’ll want to be using less than 20% of your available credit. This level of debt and less also gives the banks more faith that you can pay your home loan, even with only one good year of tax returns.

? Tip 6: Get Your Financial Reports in Order

If you’re using the one good year of tax filings strategy, you’ll need solid business financial reports as well. This is the time to get with your tax professional and make sure you can show a healthy balance sheet and a good profit and loss statement for the previous taxable year. In order to do that, you have to have your business books in order.

If your financials are a mess, or if you don’t understand what the reports show, now’s the time to dig in and figure things out.

? Tip 7: It’s Okay to Wait

Fannie Mae and Freddie Mac recently made a decision to stop accepting a 12 month look back at your financials to qualify you for a loan. That means even if your income and business looks great from March – March, you may not qualify for a loan.

As of the date of writing this article, your tax filings are the only documents that Fannie Mae and Freddie Mac will use for your personal and business income. So, if you’re showing low income or a business loss, you may need to wait another year.

Waiting a year can feel interminable. However, the wait gives you time to get your financial house in order. And that includes saving for all the things you’ll need to purchase a house.

Read about the Small Business Owner’s Home Buying Timeline here.

Filing Taxes Jointly with My Spouse

If you are married, you can file your taxes jointly with your spouse. If your spouse has enough income to qualify for a home loan, you might not need information from your taxes. And that leads us to our Bonus Tip…

? Bonus Tip: Seek Professional Advice & Communicate Your Goals

As you can see, the world of taxes gets complicated and tax regulations constantly change. In addition, your circumstances are likely unique.

You don’t have to do this alone! You don’t have to figure out how to file your personal and business taxes to qualify for a home loan. After all, you’ve got a business to run.

Our best tip for small business owners looking to buy a home is to get professional help. Speak to your tax specialist when you first begin thinking of buying a home. Get their advice from the beginning of your process of saving to buy. That way you’ll have plenty of time to get things in order and to file your taxes in a way that helps you reach your home buying goal.

Are You a Small Business Owner?

Are you a small business owner looking to buy a house? You’ve come to the right place! Here at the Mike Brown Group, we have experience working with small business owners like you. We can help you find the right lenders, tax advisors, and the home you’ve always wanted.